Copper: A Market Of Extremes

Once this phase of contraction is completed, a new cycle of growth will commence.

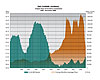

Just six months ago, on July 2, 2008, the price of copper on Comex closed at a record high $4.08 per pound. As of early December, copper was trading in the $1.35 range, down $2.73, or 67% from that historic peak with all indications suggesting it has further to fall.

There are many questions that arise from this reversal of fortune to include how and why the market rose the way it did, and just as important, what caused the precipitous fall?

Broadly speaking, one can say the roots of this bull market have their origin in 2002 following the bursting of the dot.com bubble that pushed equity prices sharply lower, coupled with the horrific attack upon the United States that sent the global economy into a downward spiral and the copper market into a near depression. That year saw global copper consumption decline by almost 200,000 metric tons, or 1.3%, the first such loss to occur in 10 years. Indeed, the severity of the downturn cannot be emphasized enough as the price of copper fell to the 60-cent range, representing a near 15-year low.

In response to weak demand, depressed prices, and excess inventories that rose to a record high 1.27 million MT in Comex and London Metal Exchange warehouses, producers slashed output in 2002 and 2003 as losses mounted.

Coincident with the actions being taken to restore market balance, consumption in China had been rising, along with their rapidly growing economy. Historically, the United States had been the world’s largest producer and consumer of refined copper. In 2002, however, the equation changed as China surpassed the United States in both production and consumption, and their appetite for metal continues to grow.

Typically, bull markets don’t begin with a bang. Rather, the early stages tend to be long-drawn-out affairs with periods of doubt that the markets will ever fully recover again. But recover it did. By the fourth quarter of 2003, inventories held in exchange warehouses had fallen some 575,000 MT, or 45% from the peak, with the price closing above the $1 level for the first time since 1997.

As 2004 got underway, it became increasingly apparent that a rising trend was developing that attracted the attention of the speculative community to include major hedge funds. One by one they climbed on board, and with vast sums of money multiplied many times over with the use of leverage, bought massive quantities of copper - causing the gradually rising slope of the price curve to begin moving vertically higher.

During the first half of 2006, it wasn’t unusual to see the price climb 10 cents in a single session, with more than a few days seeing a 20-cent advance. By May 2006, however, the copper market erupted in a dramatic ‘blow off’ top, as two major speculators with opposing views of the market fought for supremacy in a test of nerves that only one could win. By the time the battle was over, copper had soared 44 cents in one day alone, to close at $4.08 on May 23, 2006. Once the dust had settled though, the market fell back to $3.10 just a few weeks later, and by February 2007, it stood at $2.40, off 40% from the high. From this point, it appeared the bull market had run its course with expectations of lower prices ahead.

With the benefit of hindsight, however, it was not the end of the run. Throughout 2007, the concept of a long-term bull market in commodities - a ‘Super Cycle’ - was gaining credibility. The assumption was that a new world order was emerging, wherein developing economies of China, India, Brazil and Russia, among others, would have an insatiable appetite for all commodities that would hold prices aloft for many years to come. Thus, we saw prices move higher across the board to include crude oil reaching a record high $145 per barrel, while copper not only recovered all lost ground, but soared back to its previous high of $4.08.

Against this background of rising prices, however, the global economy was in turmoil. What began as a downturn in the domestic housing market, ostensibly because of sub prime mortgages, turned into a full-fledged conflagration as major financial institutions throughout the world were exposed to massive losses resulting from the proliferation of highly complex debt instruments. Almost overnight, the markets that had embraced risk with the use of easy credit suddenly became risk adverse, and the availability of credit dried up just as quickly, causing prices to collapse. During the month of October alone, copper fell more than $1 per pound, representing an unprecedented loss in value.

Today the problems facing our economy, and indeed, the global markets are many, and deeply complex. Thus, the current thinking is that prices will continue to fall until the excesses of the past several years are eliminated from the financial system. If history is our guide, however, once this phase of contraction is completed, a new cycle of growth will commence for the economy and for copper.

Copper Price & Inventory Comparison (1999 - November 2008)

Just six months ago, on July 2, 2008, the price of copper on Comex closed at a record high $4.08 per pound. As of early December, copper was trading in the $1.35 range, down $2.73, or 67% from that historic peak with all indications suggesting it has further to fall.

There are many questions that arise from this reversal of fortune to include how and why the market rose the way it did, and just as important, what caused the precipitous fall?

Broadly speaking, one can say the roots of this bull market have their origin in 2002 following the bursting of the dot.com bubble that pushed equity prices sharply lower, coupled with the horrific attack upon the United States that sent the global economy into a downward spiral and the copper market into a near depression. That year saw global copper consumption decline by almost 200,000 metric tons, or 1.3%, the first such loss to occur in 10 years. Indeed, the severity of the downturn cannot be emphasized enough as the price of copper fell to the 60-cent range, representing a near 15-year low.

In response to weak demand, depressed prices, and excess inventories that rose to a record high 1.27 million MT in Comex and London Metal Exchange warehouses, producers slashed output in 2002 and 2003 as losses mounted.

Coincident with the actions being taken to restore market balance, consumption in China had been rising, along with their rapidly growing economy. Historically, the United States had been the world’s largest producer and consumer of refined copper. In 2002, however, the equation changed as China surpassed the United States in both production and consumption, and their appetite for metal continues to grow.

Typically, bull markets don’t begin with a bang. Rather, the early stages tend to be long-drawn-out affairs with periods of doubt that the markets will ever fully recover again. But recover it did. By the fourth quarter of 2003, inventories held in exchange warehouses had fallen some 575,000 MT, or 45% from the peak, with the price closing above the $1 level for the first time since 1997.

As 2004 got underway, it became increasingly apparent that a rising trend was developing that attracted the attention of the speculative community to include major hedge funds. One by one they climbed on board, and with vast sums of money multiplied many times over with the use of leverage, bought massive quantities of copper - causing the gradually rising slope of the price curve to begin moving vertically higher.

During the first half of 2006, it wasn’t unusual to see the price climb 10 cents in a single session, with more than a few days seeing a 20-cent advance. By May 2006, however, the copper market erupted in a dramatic ‘blow off’ top, as two major speculators with opposing views of the market fought for supremacy in a test of nerves that only one could win. By the time the battle was over, copper had soared 44 cents in one day alone, to close at $4.08 on May 23, 2006. Once the dust had settled though, the market fell back to $3.10 just a few weeks later, and by February 2007, it stood at $2.40, off 40% from the high. From this point, it appeared the bull market had run its course with expectations of lower prices ahead.

With the benefit of hindsight, however, it was not the end of the run. Throughout 2007, the concept of a long-term bull market in commodities - a ‘Super Cycle’ - was gaining credibility. The assumption was that a new world order was emerging, wherein developing economies of China, India, Brazil and Russia, among others, would have an insatiable appetite for all commodities that would hold prices aloft for many years to come. Thus, we saw prices move higher across the board to include crude oil reaching a record high $145 per barrel, while copper not only recovered all lost ground, but soared back to its previous high of $4.08.

Against this background of rising prices, however, the global economy was in turmoil. What began as a downturn in the domestic housing market, ostensibly because of sub prime mortgages, turned into a full-fledged conflagration as major financial institutions throughout the world were exposed to massive losses resulting from the proliferation of highly complex debt instruments. Almost overnight, the markets that had embraced risk with the use of easy credit suddenly became risk adverse, and the availability of credit dried up just as quickly, causing prices to collapse. During the month of October alone, copper fell more than $1 per pound, representing an unprecedented loss in value.

Today the problems facing our economy, and indeed, the global markets are many, and deeply complex. Thus, the current thinking is that prices will continue to fall until the excesses of the past several years are eliminated from the financial system. If history is our guide, however, once this phase of contraction is completed, a new cycle of growth will commence for the economy and for copper.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!