2008 PREMIER 150 ― Facing Challenges

This year, as in 2007, we awarded the top spot in the Premier 150 ranking to Newport News, VA-based Ferguson, in spite of the higher sales reported by Atlanta-based HD Supply. Because we were unable to determine how much of its sales are directly related to our industry, we placed HD Supply in the No. 2 position.

According to some estimates, 2007 sales for plumbing wholesalers decreased from 5% to 15% or more in some instances, depending on their mix and location. For example, in markets like Florida and the Southwest where residential new construction - fueled by sub-prime mortgages - had overheated, wholesalers that focused mainly on residential plumbing may have seen sales decline by 30% or more.

“With new housing starts nationally dropping down by half from 2005 to 2007, there has been a substantial impact on PHCP wholesaler sales and the manufacturers they represent,” according to an industry source, who preferred to remain unidentified. “Distributors that sell HVAC, operate showrooms and/or do commercial business selling to hotels, schools and hospitals, may be experiencing a less dramatic fall-off in sales. Meanwhile, many PVF wholesalers have seen sales increases, fueled to some degree by increasing commodity prices.”

Another industry observer noted, “Copper was a major factor in the so-called growth, which was really inflation. PVF commercial construction is still very strong and that is what is keeping PVF strong. Plumbing sales have been a disaster.”

Consolidation And Cost Cutting

Acquisition and merger activity continued through 2007, but companies also closed branches, reduced work forces and took other steps to reduce overhead costs.On the acquisition and merger front, perhaps the most notable events were the sale of Atlanta-based HD Supply by The Home Depot to a group of three private equity firms comprising Bain Capital, The Carlyle Group, and Clayton, Dubilier & Rice, in July 2007 and the merger of Red Man Pipe & Supply, Tulsa, OK, with McJunkin Corp., Charleston, WV, completed in November 2007.

ACR Group, Houston, TX (No. 26 last year), was acquired by Watsco, Coconut Grove, FL, in August 2007.

Burns Cascade Co., Syracuse, NY (No. 130 last year), was acquired by F.W. Webb Co., Bedford, MA, in November 2007.

Edward B. Ward Co., South San Francisco, CA, ranked No. 68 this year based on our estimates, was acquired by Carrier Corp. in September 2007.

Wolseley/Ferguson made 22 acquisitions in North America in the 2007 fiscal year, including Ferguson’s purchase of PVF wholesaler Davidson Pipe Co., Brooklyn, NY, in August 2007. Davidson Pipe is on the list this year with estimated sales but may be removed next year.

Wolseley’s Group Chief Executive, Chip Hornsby, noted that Wolseley’s North American businesses were impacted by the rapid slowdown in the U.S. new housing market. Stock Building Supply’s sales in local currency fell 13.4% and its trading profit dropped 74.9%, Hornsby said. As a result, Stock closed about 46 branches and reduced headcount by about 20%.

Meanwhile, Wolseley’s Ferguson business unit saw sales rise 14.8%, including 5.5% organic growth, and trading profit increased 18.4%. The growth in the industrial, commercial, utilities and residential remodeling sectors more than offset the decline in new housing, Hornsby noted.

Wolseley Canada’s sales were up 2.1% and trading profit increased 0.7% as it continued to align its operations with the U.S. business structure.

The Total Market

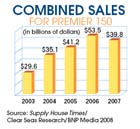

Combined 2007 sales for the companies listed as the Premier 150 were about $39.8 billion (including estimated sales and reflecting currency conversion to U.S. dollars). The substantial decrease vs. last year’s Premier 150 combined sales, which we estimated at $53.4 billion, reflects not only the decline in sales experienced by some wholesalers but also our effort to delete non-PHCP wholesale sales from the figures reported.“The housing slump really did a lot of damage and some of the largest firms were down by 10% or more in the last year,” according to an industry observer. He said that the lower sales figure estimated for this year’s Premier 150 is believable if you just consider copper tube. Plumbing industry consumption of copper tube in 2007 was down about 300 million pounds or more, according to reliable trade estimates, he noted.

“At an average 2007 Comex price of refined copper ($3.30-$3.60/lb.), the lost revenues in plumbing tube alone are about $1.1 billion at raw material (i.e., cathode) cost,” the industry observer said. The cost of fabricating the metal into plumbing tube, the manufacturer’s overhead and profit (if any), and the wholesaler’s markup to the selling price adds up to a few billion just in this one commodity material, he added.

The total PHCP wholesaling market in the United States and Canada was estimated at $67 billion, down nearly 8% from revised 2006 total industry sales of $72.8 billion. In the May 2007 issue we listed the figure $73.2 billion for the overall market in 2006 but that was adjusted down slightly in response to later revisions by the U.S. Census Bureau in its tracking of “Hardware and Plumbing” sales.

The Up Side

In last year’s survey, 81% of respondents projected their 2007 sales would increase vs. 2006. More than half - 59% - did see their sales rise in 2007. Only 10% reported a decrease, while 31% said sales were flat.Looking at the top 25 wholesalers in the 2008 Premier 150, 17 reported higher sales in 2007; six were down and two were the same. Of those in the top 25 who shared their sales breakdown, six do 50% or more of their business in PVF; six do 50% or more in HVACR and five do 50% or more in plumbing and hydronics.

The Canadian Institute of Plumbing & Heating reported that Canadian PHCP wholesalers enjoyed a 5% sales increase in 2007 and achieved another record year (sales were up 7.5% in 2006, also a record year). According to the Wholesalers’ Sales Report produced by the Profit Planning Group, all regions were up except Ontario, Quebec and Atlantic, mainly due to sales being down for PVF and waterworks. Sales of hydronics was up 9.3%; HVACR was up 7.9%; plumbing was up 7.7%; waterworks was up 7.8% for the year, but down 13% in December; and PVF was down 8.4% for the year and down 16% in December, according to the report.

Rising Stars

The 14 wholesalers that moved up 10 or more spots in the Premier 150 ranking based on their 2007 sales were (in alphabetical order):- All-Tex Pipe & Supply, Dallas, TX;

Bartle & Gibson Co. Ltd., Edmonton, Alberta, Canada;

Chicago Tube & Iron, Romeoville, IL;

Colonial Commercial Corp. (listed as Universal Supply Group last year), Hawthorne, NJ;

Ed’s Supply Co., Nashville, TN;

The Granite Group, Concord, NH;

Hirsch Pipe & Supply Co., Van Nuys, CA;

Robert-James Sales, Buffalo, NY;

Kenny Pipe & Supply, Nashville, TN;

The Macomb Group, Sterling Heights, MI;

Munch’s Supply Co., New Lenox, IL;

Murray Supply Co., Winston-Salem, NC;

Puget Sound Pipe and Supply Co., Kent, WA; and

S.W. Anderson Sales Corp., Farmingdale, NY.

- American Metals Supply, Fenton, MO (www.americanmetalssupply.com)

- Express Pipe & Supply Co., Culver City, CA (www.expresspipe.com)

- Epting Distributors, Columbia, SC (www.eptingdist.com)

- Mid-City Supply Co., Elkhart, IN (www.mid-city.com)

Other Changes

In addition to ACR Group and Burns Cascade, we have removed Bush Supply, Harlingen, TX (No. 116 last year), from the list based on its acquisition - as part of Nunn Electric Supply Co. - by Border States, Fargo, ND.Some companies that have been acquired continue to submit information to us for the Premier 150, such as EMCO Corp. in Canada, owned by Hajoca Corp., and Wolseley Canada, which is being integrated with its sister company, Ferguson.

Looking Ahead

More than half (59%) of the respondents to the Premier 150 projected a sales increase in 2008; 25% predicted a decrease in sales; and 16% said they expect flat sales.According to the forecast data the Canadian Institute of Plumbing & Heating shared with its members, the construction industry in Canada was expected to grow by 3.5% by the end of 2007 and by 3.1% in 2008. Greater growth was projected for the non-residential construction market vs. residential in both 2007 and 2008, with a 5% increase predicted for non-residential in 2008 vs. a 0.3% increase for the residential sector.

The goal of Wolseley and Ferguson is to continue to double in size every five to seven years, Group CEO Chip Hornsby said in a statement. “In the short term there needs to be more emphasis on our organic growth … putting more volume through our existing locations and taking advantage of past investments.” Acquisitions will remain a key part of the company’s strategy, he added.

A trade observer quoted industry predictions that copper supplies will tighten in the second quarter as demand quickens and the credit crunch fades; after hitting rock-bottom around May, some significant recovery is expected in the second half.

“2008 is a roll of the dice,” said one industry source. “If we have a recession we should know by May 2008. I think the turnaround will start mid-year of 2008.”

Special thanks to: Beth Shor, Kelly Johnson, Jim Olsztynski, Lydia White, Michelle Maki, Steven George, Mike Robinson, ASA and trade sources for their help.

Links

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!